urine collection container,Specimen Container, Weight Boats Taizhou TOPAID Medical Device Co,,ltd , https://www.topaidgen.com

**Abstract**

Core Tip: Overall, the current trend remains favorable for copper prices, and we maintain a relatively optimistic outlook. It is expected that next week will be a volatile period, with a support level at $7,200 and resistance at $7,500. Compared to the Shanghai copper range of 5.15-54,000, spot copper is currently trading between 5.2-5.45 million, while scrap copper is in the range of 4.7-4.9 million.

**First, the Electrolytic Copper Market**

This week, the Shanghai copper market showed a positive trend, with prices now above 53,000. Spot good copper continues to maintain its premium, as shown in the following data:

According to the chart, the spot price of Shanghai copper has been strong this week, maintaining a premium of around 250 yuan per ton. In North China, the premium is still high, approaching 400 yuan per ton, while in South China, it has dropped slightly, remaining around 200 yuan per ton or lower. The limited supply of good copper in East China has helped sustain the premium, but transactions have not increased significantly. Most of the movement comes from middlemen who are moving goods downstream for processing, with small volumes and limited orders due to the current high copper prices.

Looking ahead, we expect the premium on good copper in East China to continue rising next week.

This week, the Shanghai-London ratio performed slightly better than expected, but the increase was modest. Import losses have also narrowed, and the ratio is now fluctuating around 500 yuan per ton. This environment is slightly more favorable for copper financing. Some traders previously speculated that bonded area copper inventories had dropped to 300,000 tons, but recent data suggests that inventories fell fastest between May and July, and may rise again unless consumption improves or prices drop further.

The spot premium for copper has remained stable, reaching around $30 per ton. The price gap between Shanghai and London is small, and we expect the premium to continue in the short term. However, with the end of the month approaching, spot dealers may reduce inventory and withdraw funds, so the Shanghai-London ratio is unlikely to change much next week.

**Second, the Recycled Copper Market**

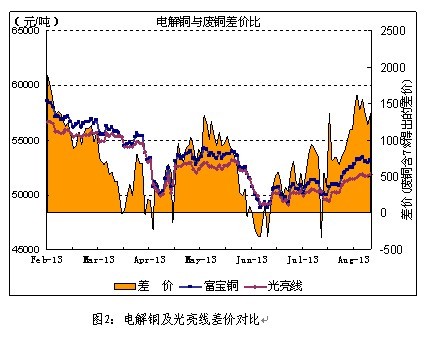

1. **Electrolytic Copper and Bright Lines**

The price of scrap copper remained largely unchanged this week, with only minor fluctuations. The actual transaction price stayed stable, with Foshan’s bright line average at around 48,400, slightly up from last week. The performance of copper prices was stronger than expected, leading to a better-than-expected scrap copper price. However, the refined price difference remains high, indicating a relative oversupply in the market.

Positive macroeconomic news, such as the Fed minutes not specifying a timeline for QE withdrawal and strong manufacturing data from China and Europe, helped prevent a market decline. From a technical perspective, copper prices are expected to remain strong, although the probability of short-term conflicts is low.

Despite the bearish sentiment in the scrap copper spot market, demand from downstream sectors has not improved significantly. Copper factories are hesitant to purchase, but the large refined price gap has provided some support for scrap copper. With the traditional "Jinjiuyin10" season approaching and the PMI data returning to above 50, there is hope for a recovery in scrap copper prices later. However, given the need for technical adjustments, we believe it's better to wait for a better opportunity to stock up rather than chase high prices. The potential impact on scrap copper prices could reach 50,000.

2. **August Cable Enterprise Demand and Capital Issues Continue**

Operating rates among 38 cable companies were mixed. Large-scale enterprises (over 10,000 tons annually) operated at an average of 72.12%, medium-sized ones (1,000–10,000 tons) at 54.76%, and small ones (under 1,000 tons) at 57.95%. Orders varied significantly, with large companies averaging 2,083.33 tons, medium ones 254.64 tons, and small ones just 18.90 tons.

High temperatures have affected construction activity, reducing demand. Payment delays are also causing capital flow issues. One cable company noted that August is typically a low season, and with weak market demand, orders have declined. They also mentioned difficulties in raw material procurement due to delayed payments. While they remain cautious about the second half of the year, they still hope for a rebound in September.

**Third, Downstream Market Analysis**

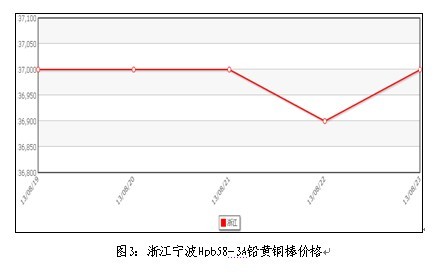

Ningbo Jinlong Hpb58-3 brass rod ex-factory price remained stable at 37,000 yuan/ton, consistent with copper trends. With copper prices in a sideways range near $7,300, market orders have not improved, and manufacturers have little room to adjust prices.

Market activity for copper products remained largely unchanged, though prices of finished products rose after two consecutive weeks of rebound. Lead brass rods are currently priced low, but demand is weak. On the other hand, small, high-quality copper rods are more active, indicating rising demand for high-precision technology products. As summer continues, copper processing companies are reducing orders, and raw material replenishment is limited. Some buyers are wary of high prices, but with "Jinjiuyin10" approaching, inventory operations are increasing. However, market concerns suggest procurement intensity will not be very high. Demand for copper products is expected to improve in September.

In the cable industry, orders over the past two months have remained stable, though operating rates have slightly declined due to off-season and hot weather. According to surveyed manufacturers, market downturns and payment delays are hindering production. Many companies faced tight capital chains due to previous price drops, and accessing bank loans is difficult. However, as the weather cools and infrastructure projects increase, cable usage is expected to rise.

**Fourth, Futures Market Analysis and Forecast**

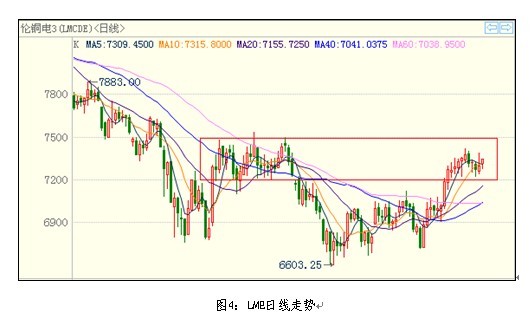

This week, copper prices rebounded from the bottom, showing a small volatility with strong support around $7,200. The chart below illustrates the trend:

From a macroeconomic perspective, the Fed meeting minutes indicated a high likelihood of slowing bond purchases in the future, which could reduce commodity risk appetite. Strong US real estate data and improving economic stability suggest that the possibility of a September QE exit is relatively low. The Fed is likely to gradually release this expectation to minimize market impact.

China’s HSBC manufacturing PMI rose above the threshold in August, and the US Markit manufacturing PMI reached a five-month high of 53.9. Although France remains weak, the Eurozone PMI hit a 26-month high, and Germany performed strongly. These positive economic indicators suggest that the global macroeconomic environment is gradually improving.

According to the Chilean Copper Industry Council, the average cost of producing electrolytic copper in 2012 was $2.22 per pound. Over the past decade, production costs in Chile have increased by 4.5 times. Investment in each ton of refined copper rose from $4.5 million in 2003 to $20.5 million in 2013. Production costs for GABY mine were $10 million per ton at the beginning of the century, but now ESCONDIDAD and QUEBRADA BLANCA mines require $35 million per ton. Increased environmental regulations and higher costs in equipment, services, and engineering have driven up mining costs, which are expected to support copper prices.

On the technical side, the bullish signals previously highlighted have been confirmed, and the market has seen a significant upward move. Positions, volume, and price are well aligned, with the moving average system still in a bull phase. Institutional investors have shown increased net long positions, suggesting improved risk appetite and continued bullish sentiment.

In summary, the current trend remains favorable for copper prices, and we maintain a relatively optimistic outlook. It is expected that next week will be a volatile period, with a support level at $7,200 and resistance at $7,500. Compared to the Shanghai copper range of 5.15-54,000, spot copper is currently trading between 5.2-5.45 million, while scrap copper is in the range of 4.7-4.9 million.