Distribution map of “80 major projects†approved by the National Development and Reform Commission

**Abstract**

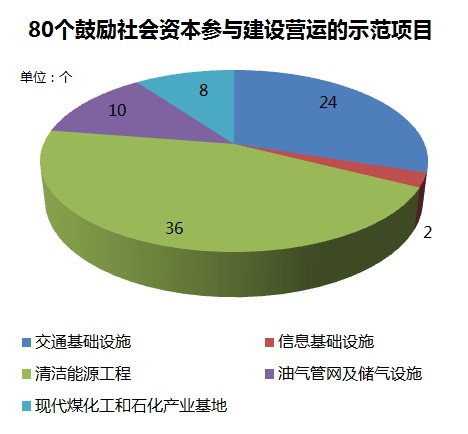

On May 21, the National Development and Reform Commission (NDRC) announced the first batch of 80 demonstration projects aimed at encouraging social capital to participate in infrastructure development. These projects span multiple sectors, including 24 transportation infrastructure initiatives, 10 oil and gas pipeline and storage facilities, 8 modern coal chemical and petrochemical industrial bases, 36 clean energy projects, and 2 information infrastructure projects. The total investment is expected to exceed one trillion yuan, signaling a major push for private sector involvement in key national projects.

Once these projects are launched, they will have a significant impact on the economy. They will immediately boost demand for construction materials, metals, and composites. Additionally, the planned production capacity of various commodities will be affected by the new energy and petrochemical projects. Therefore, understanding the geographical distribution of these 80 projects is essential for investors and stakeholders looking to capitalize on this opportunity.

Today, we’re taking a closer look at these 80 projects across five key areas.

**Transportation Infrastructure Projects**

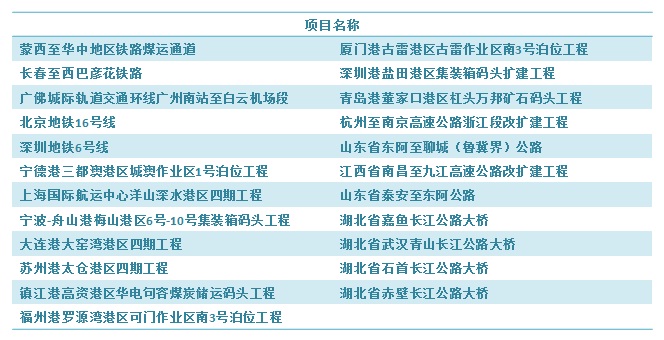

Out of the 80 projects, 24 are focused on transportation infrastructure, making up about a third of the total. The total investment in this sector is estimated to exceed 310 billion yuan. However, the level of difficulty varies significantly between different sub-sectors. For example, road and port projects have seen relatively easy access for private capital. In contrast, railway projects present a greater challenge. This is the first time that railways have been opened to private capital after the recent reform, and the entry of private players into this traditionally state-controlled sector is untested, which could lead to resistance and uncertainty.

**Clean Energy Field**

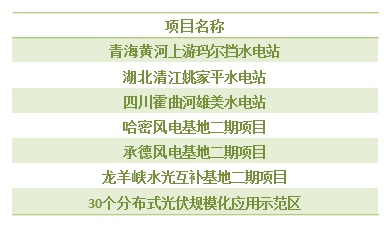

The clean energy power generation sector is another major focus area for private capital. With growing environmental concerns, China has pushed for distributed power reforms and renewable energy expansion. However, the sector still relies heavily on government subsidies. To ease financial pressure, the NDRC recently announced the inclusion of three hydropower projects, two power generation projects, and 30 distributed photovoltaic (PV) projects, aiming to attract private investment.

Despite this, private investors remain cautious, especially regarding distributed PV projects. Issues such as property rights, shared returns, and maintenance responsibilities create challenges. Additionally, the problem of self-consumption of solar power remains unresolved, leading to hesitation among private investors. If the government wants to truly stimulate private participation in this field, more supportive policies and clearer regulations will be necessary.

**Oil and Gas Pipeline Network and Storage Facilities**

China’s oil and gas pipeline network and storage facilities have long been dominated by the “three oil majors†— Sinopec, PetroChina, and CNOOC. Opening these sectors to private capital not only meets rising domestic energy demand but also signals the central government’s commitment to mixed-ownership reforms.

Sinopec was the first among the three to introduce private capital into its pipeline and storage systems. This includes high-profile projects like the Tianjin LNG receiving station, which could become the first officially approved LNG terminal project involving social capital. This move sends a strong signal of market openness.

PetroChina, although slower in implementing mixed-ownership reforms, has taken significant steps this time. It has opened six oil and gas pipelines and storage projects, including the critical middle section of the West-East Gas Pipeline, highlighting the importance of private capital in its strategy.

CNOOC, while also engaging in mixed-ownership reforms, has fewer pipeline and storage assets compared to its competitors. As a result, it hasn’t opened any projects in this sector to private capital yet.

Despite these positive developments, many in the market remain skeptical. Large-scale gas transmission projects require substantial investment, and private capital may lack the financial resources needed to compete effectively. Even if they enter, they may struggle to gain influence in the long run.

**Modern Coal Chemical and Petrochemical Industrial Bases**

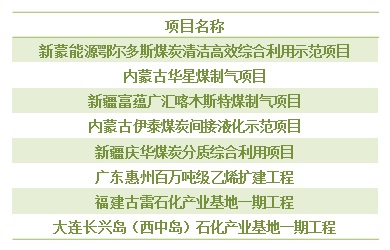

Similar to the oil and gas sector, coal chemical and petrochemical industrial bases are largely controlled by state-owned enterprises. However, compared to the large-scale investments required for pipelines and storage, these projects generally require less capital, making them more accessible to private investors.

One of the most notable projects in this category is the CNOOC Guangdong Huizhou million-ton ethylene expansion project, indicating that CNOOC has also joined the mixed-ownership reform movement.

**Information Infrastructure**

Among the five open sectors, information infrastructure stands out as the only one without specific construction projects listed. However, it remains a highly attractive area for private investment. Western countries have long embraced privatization in this field, offering valuable lessons for China.

Private capital entering the information infrastructure sector may face fewer technological barriers, but the real challenge lies with the existing three major operators: China Telecom, China Mobile, and China Unicom. Whether they are willing to embrace ownership reforms will ultimately determine the success of private investment in this sector.

Led Outdoor Bollard Light,Solar Led Bollard,Led Garden Bollards,Pillar Light

Ningbo Royalux Lighting Co., Ltd. , https://www.royaluxlite.com