Distribution map of “80 major projects†approved by the National Development and Reform Commission

**Abstract**

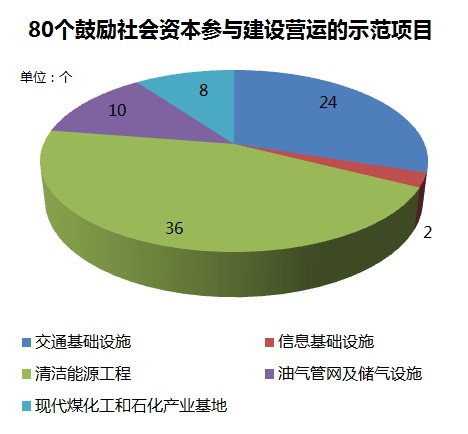

On May 21, the National Development and Reform Commission (NDRC) announced the first batch of 80 demonstration projects aimed at encouraging social capital to participate in infrastructure construction and operations. These projects span various sectors, including 24 transportation infrastructure projects, 10 oil and gas pipeline networks and gas storage facilities, 8 modern coal chemical and petrochemical industrial bases, 36 clean energy projects, and 2 information infrastructure projects. The total investment is estimated to exceed one trillion yuan, marking a significant step in China’s push for private sector involvement in key economic areas.

Once these projects are launched, they will have a substantial impact on the demand for building materials, metals, and other related industries. Additionally, the planned production capacity of certain commodities may be affected, especially in the petrochemical and energy sectors. As such, understanding the geographical distribution of these 80 projects is crucial for stakeholders and investors alike.

Today, we take a closer look at the 80 projects across five key sectors.

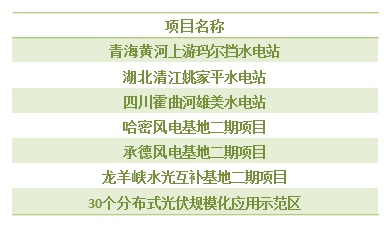

The clean energy power generation sector is another key area for private capital. With growing environmental concerns, China has been pushing for distributed power reform and clean energy development. However, the sector still relies heavily on government subsidies. To reduce financial pressure, the NDRC recently opened three hydropower projects, two power generation projects, and 30 distributed photovoltaic projects to private investors.

Despite this, private capital remains cautious, particularly in the distributed photovoltaic power generation field. Issues such as complex property rights, return sharing, and maintenance challenges make the sector less attractive. Additionally, self-use difficulties for solar power further deter investment. For the government to truly encourage private participation, more supportive policies and clearer regulations will be needed.

The clean energy power generation sector is another key area for private capital. With growing environmental concerns, China has been pushing for distributed power reform and clean energy development. However, the sector still relies heavily on government subsidies. To reduce financial pressure, the NDRC recently opened three hydropower projects, two power generation projects, and 30 distributed photovoltaic projects to private investors.

Despite this, private capital remains cautious, particularly in the distributed photovoltaic power generation field. Issues such as complex property rights, return sharing, and maintenance challenges make the sector less attractive. Additionally, self-use difficulties for solar power further deter investment. For the government to truly encourage private participation, more supportive policies and clearer regulations will be needed.

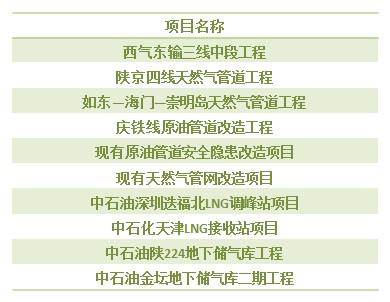

China's oil and gas pipeline network and gas storage facilities are traditionally dominated by the "three major oil companies." Opening these sectors to private capital not only meets rising domestic energy demands but also signals the central government’s commitment to mixed-ownership reforms.

Sinopec was the first among the three to introduce private capital into its operations. This time, it opened three oil and gas pipelines and gas storage facilities, including the high-profile Tianjin LNG receiving station project. This could be the first official LNG terminal project involving social capital, signaling a shift in market access.

Although PetroChina started its mixed-ownership reforms later than Sinopec, it has made strong progress. It opened six oil and gas pipelines and gas storage facilities, including the West-East Gas Pipeline’s middle section, highlighting the importance of private capital in this sector.

CNOOC, while also pursuing mixed-ownership reforms, has fewer pipeline and storage resources compared to its rivals. As a result, it hasn’t opened many projects in this area yet.

Despite the positive steps, many remain skeptical. Large-scale gas transmission projects require massive investments, which most private investors may not be able to afford. Even if they do enter, their influence in operations may be limited.

China's oil and gas pipeline network and gas storage facilities are traditionally dominated by the "three major oil companies." Opening these sectors to private capital not only meets rising domestic energy demands but also signals the central government’s commitment to mixed-ownership reforms.

Sinopec was the first among the three to introduce private capital into its operations. This time, it opened three oil and gas pipelines and gas storage facilities, including the high-profile Tianjin LNG receiving station project. This could be the first official LNG terminal project involving social capital, signaling a shift in market access.

Although PetroChina started its mixed-ownership reforms later than Sinopec, it has made strong progress. It opened six oil and gas pipelines and gas storage facilities, including the West-East Gas Pipeline’s middle section, highlighting the importance of private capital in this sector.

CNOOC, while also pursuing mixed-ownership reforms, has fewer pipeline and storage resources compared to its rivals. As a result, it hasn’t opened many projects in this area yet.

Despite the positive steps, many remain skeptical. Large-scale gas transmission projects require massive investments, which most private investors may not be able to afford. Even if they do enter, their influence in operations may be limited.

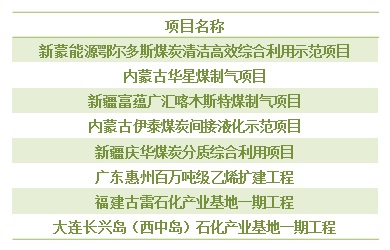

Similar to the oil and gas sector, coal chemical and petrochemical industrial bases are largely controlled by state-owned enterprises. Compared to pipeline and storage projects, these base projects require less investment and have lower entry barriers, making them more attractive to private capital.

One of the most notable projects in this category is the CNOOC Guangdong Huizhou million-ton ethylene expansion project, indicating that CNOOC has also joined the mixed-ownership reform movement.

Similar to the oil and gas sector, coal chemical and petrochemical industrial bases are largely controlled by state-owned enterprises. Compared to pipeline and storage projects, these base projects require less investment and have lower entry barriers, making them more attractive to private capital.

One of the most notable projects in this category is the CNOOC Guangdong Huizhou million-ton ethylene expansion project, indicating that CNOOC has also joined the mixed-ownership reform movement.

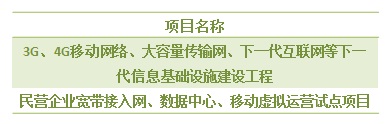

In the five sectors opened to private capital, information infrastructure is the only one without specific construction projects mentioned. However, it remains a highly attractive area for private investment.

Western countries have long embraced privatization in this sector, offering valuable lessons. Technologically, private capital should face few barriers. The main challenge, however, lies with the existing telecom monopolies—China Telecom, China Mobile, and China Unicom. Whether they are willing to embrace ownership reform will determine the success of private investment in this area.

In the five sectors opened to private capital, information infrastructure is the only one without specific construction projects mentioned. However, it remains a highly attractive area for private investment.

Western countries have long embraced privatization in this sector, offering valuable lessons. Technologically, private capital should face few barriers. The main challenge, however, lies with the existing telecom monopolies—China Telecom, China Mobile, and China Unicom. Whether they are willing to embrace ownership reform will determine the success of private investment in this area.

80 Items Overview

Transportation Infrastructure Projects

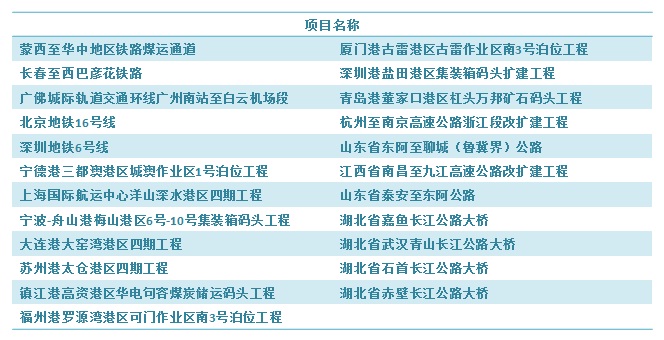

Among the five sectors opened to private capital, transportation infrastructure accounts for 24 out of the 80 projects, making up about a third of the total. The overall investment in this sector is expected to exceed 310 billion yuan. However, the difficulty of investing in specific projects varies significantly. In sectors like roads and ports, private capital has already been involved, making investment relatively easier. Railways, however, present a different challenge. This marks the first time that private capital is entering the railway sector following recent reforms. While this is a positive move, the process is still untested, and there are likely to be significant obstacles along the way.

Clean Energy Field

Modern Coal Chemical and Petrochemical Industrial Bases

Information Infrastructure

Led Outdoor Bollard Light,Solar Led Bollard,Led Garden Bollards,Pillar Light

Ningbo Royalux Lighting Co., Ltd. , https://www.royaluxlite.com